Tuesday, September 29, 2009

Is Gold A Reasonable Investment?

This essay rounds up arguments for gold as a reasonable investment.

China

Commentators such as Ambrose Evans-Pritchard and Byron King argue that China's hunger for gold will put a floor on gold prices.

Specifically, they argue that China will "buy the dips" in gold prices, effectively putting a minimum on how low gold prices can go.

Inflation

It is conventional wisdom that gold is a hedge against inflation.

For example, noted inflationist John Williams advises buying gold.

Axel Merk argues that gold is a better buy than TIPS as an inflation bet.

And Taleb advised buying gold in May, since currencies including the dollar and euro face pressures.

Deflation

If gold does well during times of inflation, it makes sense that it would perform poorly during deflationary periods.

But Examiner.com points out that such an assumption is probably untrue.

Specifically, as Examiner.com writes:Eric Sprott - who manages $4.5 billion in assets, and correctly predicted in March of 2008 a "systemic financial meltdown” - says:“I believe no matter what environment you’re in - deflation or inflation - people will run to gold,” Sprott said. “Gold is proving exactly what we all would have expected, that in almost any environment, it’s a go-to asset.”And investment analyst and financial writer Yves Smith argues that gold does well during both periods of deflation and high inflation. She argues:

Historically, gold does well [in] hyperinflation and deflationary [periods]. Gold does poorly under more normal conditions, and gets hammered in disinflationary conditions, a falling but positive rate of inflation.

Analyst Adrian Ash argues that gold's value actually increases during periods of deflation even if its price drops:

Does the price of gold rise or fall in a deflation?Hint: It’s a trick question, already tripping up plenty of would-be advisors...

Absent the money-supply limits which the gold standard imposed on the world, people rightly guess that double-digit inflation would prove rocket-fuel for the bull market in gold. Yet the purchasing power of gold nearly doubled during the Great Depression, and it’s risen four-fold during this decade’s low consumer-price inflation as well.Why? Because both those periods of low price-inflation saw the money-issuing authorities devalue the currency, first with explicit reference to gold but now without daring to name it. Roosevelt in the mid-30s slashed the dollar’s gold content by 40%; the Greenspan/Bernanke Fed devalued the Dollar again to sidestep a DotCom Depression, keeping real interest rates at less than zero, between 2002-2005.

The maestro’s apprentice applied the same trick in the back-half of 2008, but so far to no avail. And now even the European Central Bank is pumping out money – a near half-trillion euros today alone – in a bid to revive bank lending, swamp the currency markets, and pull Germany out of its first flirt with deflation since the 1930s.

Just such a devaluation – and again, absent any stated reference to gold – was attempted by the Bank of Japan a little less than a decade ago.

Indeed, Japan is the only developed nation since the end of the gold standard to have suffered an extended deflation in prices. So far, at least. Germany and Switzerland look set to try for a re-wind, and unless the dollar can outpace the euro’s descent, we might yet see truly sub-zero inflation in the United States, too.

But whatever that should mean for gold prices, all other things being equal, just doesn’t matter. Because the gold price will not get a chance. All other things are not equal, and the policy solution – rank devaluation – can only make gold more appealing to investors and savers, whether the “monetarist experiment” of TARP, quantitative easing or a half-trillion euros proves successful or not.

Japan’s slump into deflation coincided with the Bank of Japan’s “zero interest rate policy” (ZIRP) at the start of this decade. It also saw the gold price worldwide hit rock-bottom and turn higher, a move that analysts (including us) have typically linked to US monetary moves and investment cash looking for safety as the Dotcom Bubble exploded.

But zero-rate money from the world’s second-largest economy shouldn’t be ignored. And today, zero-rate money is all the developed world has to offer – a trick that might not beat deflation, but might just spur a whole new rush into gold.

In other words, Ash argues that you can't take inflation or deflation in a vacuum. During deflationary periods - like we have now - governments always increase the money supply with a flood of new dollars, which is bullish for gold.

And PhD economist Marc Faber wrote in October 2007 that gold will do well even in a deflation:

How would gold perform in a deflationary global recession? Initially gold could come under some pressure as well but once the realization sinks in how messy deflation would be for over-indebted countries and households, its price would likely soar.

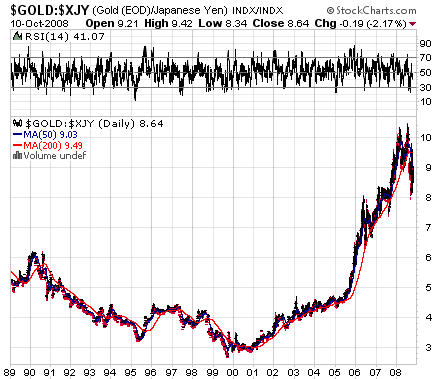

Therefore, under both scenarios - stagflation or deflationary recession - gold, gold equities and other precious metals should continue to perform better than financial assets.Looking At the Charts

Is Faber right?

Well, take a look at the following charts showing gold's performance as compared to the yen during Japan's "lost decade" of deflation:

Japan's deflation didn't definitively end until 2007 or 2008.

This provides some evidence that gold may tend to hold or increase its value at least in the later part of the deflationary period as compared with the relevant national currency.

Moreover - approximately half the time - gold has risen during recessions in the United States:

(The grey vertical bars show periods of recession; the chart gives gold prices in monthly averages; click here for larger image).

If you study the above chart, you will see that gold seems to often fall during the beginning stages of a recession, then rise in the later stages of the recession (before 1971, the dollar was still backed by gold at a fixed price, and so gold did not fluctuate).

But what about Ash's theory?

The American Enterprises Institute notes:

After five years in a deflationary economic wilderness, the Bank of Japan switched during the spring of 2001 to a policy of quantitative easing--targeting the growth of the money supply instead of nominal interest rates--in order to engineer a rebound in demand growth.Look again at the first gold chart for Japan, above. Gold appears to start increasing against the Yen in 2001.

This may provide some evidence for Ash's thesis that it is an expansion of the money supply which pushes the price of gold up in the later stages of deflationary periods.

Uncertainty

Finally, Chris Martenson argues that - in prolonged periods of deflation - we usually see failures of large and significant banks, institutions, and perhaps even states and countries. Because gold traditionally does well during periods of uncertainty, Martenson likes gold during periods of deflation.

Examiner.com notes in a subsequent article:

Global Short Term Interest Rates Are LowMerrill Lynch agrees.

Specifically, PhD economist Nouriel Roubini paraphrases a report from Merill Lynch (not available online) as follows:

Short-term rates of 0% are bullish for gold, which serves as a store of value but is a useful hedge against deflation as well, since deflation is inherently destabilizing for financial assets. In the 2001-03 deflationary period, gold rose more than 30%, not to mention the prospect of a return to a dollar bear market. "Gold is inversely correlated to global short-term interest rates and there is a race right now towards 0%. Production is down 4.0% y/y while fiat currencies globally are being created at a double digit rate by the world's central banks....As for all the talk of a 'gold bubble,' it would take a nearly 625% surge in gold to over US$6,000/oz and a flat stock market to actually get the ratio of the two asset classes back to where it was three decades ago when bullion was in an unsustainable bubble phase."

Gold tends to be less sensitive to global economic slowdown than industrial metals or energy and works better as a hedge against crisis than inflation.

The above-quoted Merrill article states:

Gold is inversely correlated to global short-term interest rates and there is a race right now towards 0%.This argues for gold.

Polls Show Distrust in Government

Time Magazine writes:

Traditionally, gold has been a store of value when citizens do not trust their government politically or economically.

Given the enormous levels of distrust in the government politically and/or economically (and the fact that some have warned of recession-induced violence), gold might do well.

Greenspan and Exeter

Professor Emeritus of Mathematics Antal Fekete has argued for years that gold is the ultimate - and only - safe haven when things really hit the fan.

For example, in 2007 Fekete wrote:

The grand old man of the New York Federal Reserve bank’s gold department, the last Mohican, John Exter explained the devolution of money (not his term) using the model of an inverted pyramid, delicately balanced on its apex at the bottom consisting of pure gold. The pyramid has many other layers of asset classes graded according to safety, from the safest and least prolific at bottom to the least safe and most prolific asset layer, electronic dollar credits on top. (When Exter developed his model, electronic dollars had not yet existed; he talked about FR deposits.) In between you find, in decreasing order of safety, as you pass from the lower to the higher layer: silver, FR notes, T-bills, T-bonds, agency paper, other loans and liabilities denominated in dollars. In times of financial crisis people scramble downwards in the pyramid trying to get to the next and nearest safer and less prolific layer underneath. But down there the pyramid gets narrower. There is not enough of the safer and less prolific kind of assets to accommodate all who want to "devolve”. Devolution is also called "flight toDarryl Schoon makes the same argument.

safety”.

Here's a visual depiction Exeter's inverted pyramid, courtesy of FOFOA:

(Click here for full image; I am not certain every level of the pyramid is accurately ranked)

Alan Greenspan has just lent some support to the theory. Specifically:

Gold prices that jumped above $1,000 an ounce this week are signaling that investors are buying metals to hedge against declines in currencies, former Federal Reserve Chairman Alan Greenspan said.

The gains are “strictly a monetary phenomenon,” Greenspan said today at an investment conference in New York. Rising prices of precious metals and other commodities are “an indication of a very early stage of an endeavor to move away from paper currencies,” he said...

“What is fascinating is the extent to which gold still holds reign over the financial system as the ultimate source of payment,” Greenspan said.

In other words, Greenspan is saying that investors are moving out of the second-to-lowest step on the pyramid (currencies and government bonds) and into the lowest step (gold).

Are Exeter, Fekete and Schoon right? I don't know. And Greenspan might be wrong, or trying to excuse weakness in the dollar (as opposed to all paper currencies).

Note 1: Zero Hedge alleges that newly-declassified federal documents prove that gold prices have been manipulated for decades. If these documents are authentic (I have no reason to doubt their authenticity, but have no inside knowledge), if the claims of artificial price suppression are true, if this is widely publicized, if such publicity causes someone like Congressmen Alan Grayson, Brad Sherman, Ron Paul, or Dennis Kucinich to raise a ruckus in Congress, and if Congress as a whole votes to ban such a practice, then the price of gold would presumably rise. That's a lot of ifs.

Note 2: Some of the best recent arguments I've heard against investing in gold are written by Vitaliy Katsenelson. Read this, this, this and this.

Note 3: I am not an investment advisor and this should not be taken as investment advice.

7 comments:

→ Thank you for contributing to the conversation by commenting. We try to read all of the comments (but don't always have the time).

→ If you write a long comment, please use paragraph breaks. Otherwise, no one will read it. Many people still won't read it, so shorter is usually better (but it's your choice).

→ The following types of comments will be deleted if we happen to see them:

-- Comments that criticize any class of people as a whole, especially when based on an attribute they don't have control over

-- Comments that explicitly call for violence

→ Because we do not read all of the comments, I am not responsible for any unlawful or distasteful comments.

{kind=link}

{kind=link}

Don't be a fool.

ReplyDeleteGold sits idle in large vaults and small safes everywhere all over the world. It adorns the necks, fingers and toes of a lot of women in the world.

There is imaginary gold on the balance sheet of almost every gold trader too. And there is more of both the real stuff and the fake stuff being created every day.

Gold is a racket.

Gold is a highly leveraged "investment" too, just like oil. Both oil and gold are extremely susceptible to spikes and cliffs, fraud and stealth, -and rapier-like market manipulation.

You are in over your head with some real rascals when you play the gold game.

The difference between the dynamic market constraints of gold and oil is, there is -more or less steady- consumption of oil. There is very little consumption of gold.

At any price, and certainly no less especially at $1000 an ounce, gold is an almost purely speculative commodity. -And gold futures are as speculative an investment as can be made on an almost purely speculative commodity.

Think about all that for a second, Jim Rogers, shu-ee-gumbo-tui. Have another Highball too.

So then... If you are buying gold as an "investment", what are you really buying?

You are buying an almost purely speculative commodity traded in a highly leveraged marketplace, -a marketplace loaded with a wide variety of unscrupulous sharks attracted by the glitter of the yellow metal.

Remember "Treasure Island", Long John Silver, the flintlock pistols and the parrot?

And for such an obviously untenable risk, the potential return might be?

"Investors" in gold are entirely at the mercy of human psychology, -the thundering stampedes of panic -and- the irrational exuberance of greed that lured them into this pretty yellow package of the too often the self-inflated sense of being smarter than the next guy.

Yea. Buy gold. Buy gold at a thousand dollars an ounce. That makes a hell-of-a-lotta-sense to me too. Sure it does.

Have any of you ever watched your wife get dressed?

"Fickle" is the only static universal in human psychology, -on again, off-again -FICKLE!

Gold has not been a unit of monetary measure in going-on half-a-century.

Gold was dropped as a unit of monetary measure precisely because it no longer worked, -because it was too susceptible to panic and manipulation.

The price of gold is no longer determined by its monetary value in any pecuniary or currency sense.

The price of gold is determined today by the demand for gold caused by a seemingly endless stream of marketing hype, -and by the all-too-easily manipulated supply of gold, -which is an ever present sword of Damocles hanging over the head of everyone who "invests" in gold today.

Don't say YOU weren't warned, fool.

Someone is out there massively shorting gold, and all they have to do is cause a gold panic to reap immense reward from all the brilliant chicken-yellow gold "investors" who will do anything to get out of gold when the price drops -the way the price of gold CAN drop.

And the price of gold can really drop too, King Midas.

What is investing all about? From the perspective of wealth, which is interested in asset preservation and increase, the question is always a relative one. People of means don't put all their assets in one basket. They diversify based on expectations. So the question is not whether to hold gold and precious metals, but what percentage of one's portfolio should they be, considering wealth preservation and increase in terms of current expectations.

ReplyDeleteGold, as Greenpspan and others observe, has the ultimate "moneyness," Therefore, it is the medium of choice for wealth preservation. Most sophisticated investors don't buy gold for alpha, they buy it for beta, especially when circumstances indicate that gold is a safer "stash" than cash or T bills.

Gold is not only a hedge against currency fluctuations in parlous times. Gold is also a hedge against uncertainty (unknown unknowns) in contrast to ambiguity (calculable risk). For this reason, I recommend assessing the value everything else relative to (an ounce of) gold as the most reliable standard of monetary worth.

Gold is hoarded in deflationary times, and it is also sought as a hedge against inflation in inflationary times. Gold has been a pretty constant hedge against long term inflation since 1971, and therefore, it should have a place in the portfolio of anyone having enough wealth to diversify. This is usually on the order of 10-20%. However, gold only performs strikingly at the margins, where disequilibrium threatens.

The global economy hangs between deflation caused by debt destruction and inflation to counter it brought by the action of central banks. So it is not a matter of inflation or deflation at the moment. The consideration is hedging against uncertainty in times where disequilibrium could arise from a variety of factors, and the global economy remains inherently unstable. In such times, one might increase gold holdings to 50% or more.

well...sorry...I haven't read ur content yet...however.. the answer to yur "title" is...DEFINATELY!!!! HOLY SWEET JUSES YES!!!!!!!

ReplyDeleteGold is speculative game....Tell that to the Icelanders...

ReplyDeleteChina is one of the major economic power in the world, but gold investment can be tricky.

ReplyDeleteTo the first Anonymous poster in this comment thread:

ReplyDeleteSir, YOU are the fool. And a fool indeed. A jester even!

Are you a court jester for the "kings" in their paper palaces? You clearly seem to have some interest in defaming their greatest enemy: SOUND MONEY.

Look for a moment, at your own foolish statements:

You said: "Gold has not been a unit of monetary measure in going-on half-a-century."

Ooooh. Yes. You win the prize behind door number One! Which is: Half a century of the Austrian Business Cycle directly implicating the tyrannical paper money system enforced by legal tender laws and military force in the globe.

Further, despite your cry of victory that "gold has not been used for half a century", I reply simply that it WAS for over 3,000 years.

You have an example time of 1.6% of gold's timeline.

THEN you remarked, so brilliantly: "Gold was dropped as a unit of monetary measure precisely because it no longer worked, -because it was too susceptible to panic and manipulation."

Sure. Gold was dropped. In 1971! AFTER we fooled the world into accepting the dollar *in lieu* of gold, being BACKED BY Gold!

And your reason for this was to end panic and manipulation? Is this, indeed, what has happened?

WOW. What a tool.

I wouldn't say gold is speculative game at all. It is a tool to protect your wealth, not to speculate.

ReplyDelete